Time-Cost Trade-off Relationship for a Typical Job

Time-Cost Trade-off Relationship for a Typical Job

The Cost Consideration

The CPM was developed to solve the scheduling problems in an industrial setting. It was more concerned with the costs of scheduling and how to minimize them. Most jobs can be reduced in duration if extra resources are assigned to them. If the other advantages outweigh the additional cost, then the job should be expedited or crashed. But it is not necessary to crash all jobs to get a project done faster; only the critical jobs need be expedited. The CPM attempts to solve the problems of finding such jobs and how to crash them.

Schedule-Related Project CostsThe cost of a project is due to the direct costs associated with individual activities and the indirect expenses such as managerial services, indirect supplies, equipment rentals etc. Normally the direct costs related to an activity will increase if we crash that activity. On the other hand, the indirect costs decrease if the activity is shortened.

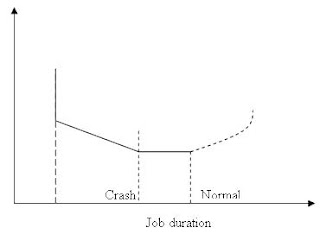

The relationship can be expressed by a straight line on a graph plotting job duration versus cost. The steeper the slope of this line, the higher the cost of expediting the activity. A horizontal line, then, indicates that crashing the job would result in no decreased efficiency shortening is possible (either because the job duration cannot be reduced further or because some other job has become critical on a parallel path). If there are parallel critical paths, then one job in each of them must be chosen for crashing. The improvements are made in a stepwise fashion and the new schedules are continued as long as the jobs can be crashed with a net reduction in total costs.

Basic Concepts of Network Cost SystemsThe basic concept of PERT and CPM cost systems is different from that of most cost accounting systems. In essence it is: Costs are to be measured and controlled primarily on a project basis rather than according to the functional organization of a firm. The rationale of the system is the entirely logical notion that responsibility for expenditures should coincide with responsibility for managing that which gives rise to the expenditures. Under a PERT or CPM management system, project managers and submanagers are ordinarily chosen for supervising individual activities and they should be responsible for controllable costs associated with the activities.

A project-oriented cost accounting system does not necessarily replace existing systems based on organizational structure. If the costs are identified with the proper degree of detail, cost summaries can readily be generated on either basis.

Cost Accounting by Work PackagesIf a project has been broken down into activities small enough to be used for purposes of detailed planning and scheduling, many such activities would be too small to be used and, therefore no added cost. If a job cannot be shortened regardless of extra resources applied to it, the line would be vertical. All the three possibilities are represented in figure 3.2.

There is probably a minimum duration which cannot be reduced no matter what the expenditure of resources (vertical portion of line). Similarly, slowing the job will decrease the costs only upto a certain point; beyond this no additional savings are obtained (horizontal portion of line).

The Lowest-Cost schedule

The CPM model specifies a method for finding the optimum point representing the lowest-cost schedule. A preliminary schedule is generated in which all jobs are assigned at their early start times and with normal resources. The length of this maximum duration schedule can be reduced only by expediting one or more of the critical path activities at an extra cost.

At each step of the process, the cost-time slope of each critical job is examined, and the job with least slope is determined. This job is expedited upto the point where no further conveniently for cost-control purposes. If so, several related activities may be grouped together into larger "work packages". These represent particular units of work for which responsibility can be clearly defined and which are still small enough to be manageable for planning and control purposes. The work packages formed at the lowest level of breakdown, then, constitute the basic unit in the PERT cost system by which actual costs are (1) collected and (2) compared with estimates for purposes of cost control.

Forecast of Project Costs

For planning and budgeting purposes, it is useful for a manager to know the time pattern of the expenditures. If costs are estimated for each work package then a projection of costs can easily be made. To do this, the assumption is usually made that expenditures for an activity are incurred at a constant rate over the duration of the activity. If this assumption is not valid for certain activities, they should be divided into a sequence of two or more activities, each having a constant expenditure rate.

A schedule graph, in which the network is plotted on a time scale and in which the horizontal length and placement of activity arrows indicate activity duration and schedule, facilitates cost calculation. When cumulative costs are plotted versus time, the graph illustrates the budget implications of early start and early finish times. The area between these two curves represents a range of budgets which are feasible from a technological viewpoint.

Analysis and Control of Project Costs

The first step in the control procedure is the measurement and recording of costs which are incurred as the project progresses. At the same time that costs are reported, an estimate should be made of the percentage of work accomplished. With the cost and time data collected from period to period as the project progresses, some very useful graphic reports are produced that help the managers to answer such questions as :

Is the project on schedule?

How far over budget are the present costs?

What are the sources of delay and overruns?

Accounting Problems with PERT/Cost

The managerial benefits from the PERT/Cost system derive largely from the increased detail with which the costs are categorized and reported. Although this detail permits closer control of project performance and costs, it is also the cause of some accounting problems. More specific of them include the following:

· Indirect Costs: Some project costs are not easily identifiable with end items or specific work packages. Conventionally, such items are considered to be a part of the overhead.

· Overhead Control: Since overhead is a sizable expense, and since overruns may result from indirect as well as direct costs, it seems desirable to provide some means of exerting better control over overhead.

· Material Costs: Because of long lead time between release of material requirements and their eventual use, actual costs of materials are often incurred long before the work packages are scheduled to begin.

{kind=link}